There’s living the conformist life. Then there’s living the non-conformist life. And, some might argue, it’s impossible to live in between the two, but it is—that’s where malicious compliance comes in. And that’s the best kind of living.

This conformist-non-conformist introduction is brought to you (not really) by this Reddit post about exactly that—sticking it to the man whenever you can, and in this case, the man is a bank with an agenda to assert dominance over a client in the form of account closure fees and the client proceeding to dance to the bank’s flute, but not an account closure jig, but a let’s keep this account active, but not really number.

More Info: Reddit

If you can’t close an account, why not keep it as inactive as possible without actually making it inactive

Image credits: Nenad Stojkovic (not the actual image)

So, Redditor u/Creepy-Analyst shared a story of how he wanted to close an inactive bank account, but the bank did what banks do and slapped a fee on it. So, instead of conforming, he went the other route.

Specifically, OP moved from Pennsylvania to Michigan some time ago. One of the things that were, alas, left unattended was his bank account. Well, OK, it was kinda sorta left tended to, in the form of transferring nearly all of its contents to another account he’s using in Michigan. The account balance left was $1.31.

Two years went by, the account was left untouched, and OP got a notice about it. Apparently, the bank was doing some housekeeping and wanted folks with inactive accounts to incur an inactivity fee, or get the account closed. Fine, OP sought out the latter option.

After all, there is a $5 closing fee, so why would you want to close it, if you can simply “keep up appearances” every 2 years and just live your life in the meantime

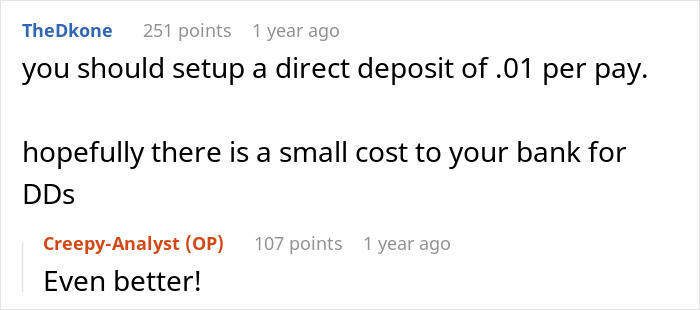

Image credits: u/Creepy-Analyst

Image credits: Steven Pisano (not the actual image)

Surprise, surprise, 3 customer support consultations later, the bank wanted a closing fee. $5. No way out: you gotta pay one way or another. Unless… you continue using your account the way the bank deems it as use. Which technically means making at least one transaction within a span of 2 years.

Cue malicious compliance.

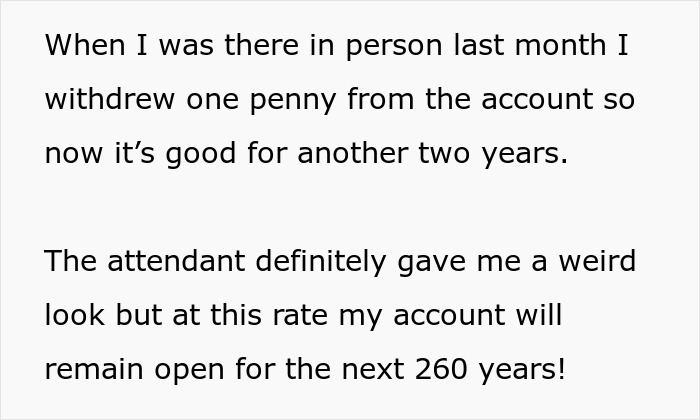

If it’s a case of making a move—any move—once every 730 days, then so be it. OP requested to withdraw 1 cent. The bank employee definitely gave a weird look, but fulfilled OP’s request regardless.

This Redditor maliciously complied with the bank’s 2-year activity rule, and started a withdrawal of a penny every 2 years from his original $1.31 balance

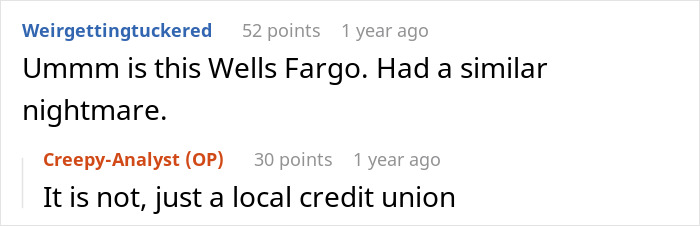

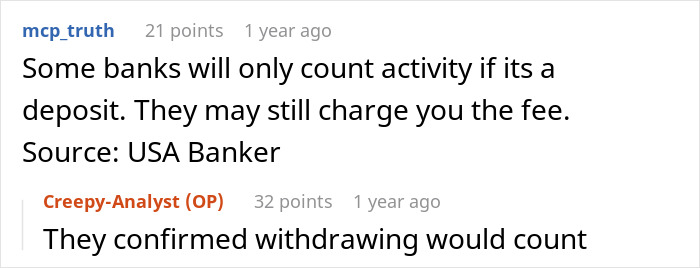

Image credits: u/Creepy-Analyst

Image credits: Paulo O (not the actual image)

It seems there are no money withdrawal fees, which makes it even better. Heck, OP could have simply withdrawn the penny and deposited it back just because he could. All he truly had to lose was time, but this was no longer an issue of time, most would wager.

Whatever the case, OP was set for another 2 years. And at this rate, if he was to continue withdrawing a penny every 2 years, he could technically have the account without incurring any fees for another 260 years. Granted, that’s if the bank does not change its monetary policy.

Realistically, no human being could live that long, but it’s nice to know that this account can, in theory, still be active under the current rules until the year 2282—a good 121 years after the events of the post-apocalyptic world of Fallout.

Folks couldn’t agree more that it is a nice plan of action—one that could be one-upped by immediately depositing said penny back

Fun fact, while there doesn’t seem to be information about the oldest account in the world, you can bet it will probably be in the oldest bank by proxy, the Banca Monte dei Paschi di Siena in Italy. It was originally founded in 1472 (that’s 689 years before the events of… you know what, never mind) and established in its present form in 1624. In 2021, it reported nearly 3 billion Euro in revenue.

Anywho, folks on Reddit enjoyed this short, but good story. Maliciously compliant indeed. The post managed to get nearly 30,000 upvotes and over 40 Reddit awards.

As you would expect, folks in the comments were everything from devious to curious. Curious because people were interested in things like why a penny, if there are talks of eliminating it altogether (turns out, just any smallest coin will suffice), and what bank it was (local credit union).

And devious because remember the whole idea of depositing the penny right back into the account as soon as you withdraw it? Yeah, that was the Redditors suggesting that.

According to this one user, banks can impose inactivity fees to encourage people to close their accounts, but if that gets ignored, they simply close it and that’s it. So, OP doesn’t necessarily have to play this game, but it’s good he’s doing it. Makes life more fun.

You can read this and more in context here. Or you can read other banking stories we’ve covered in the past here and here. And if that doesn’t sate your appetite, you’re welcome to raid the comment section where I’m sure folks will share their own banking stories, or advice on how to go about closing an account in the most malicious way possible [wink, wink].

The post Bank Doesn’t Let Guy Withdraw His .31 Easily, He Decides To Drown Them In Perpetual Transactions Over 260 Years first appeared on Bored Panda.

from Bored Panda https://ift.tt/Yj8rM2X

via IFTTT source site : boredpanda